ACCA新大纲解析(F3)

- 2014年08月22日

- 11:52

- 来源:未知

- 阅读:(128)

2024ACCA备考资料

- 财务英语入门

- 历年考题答案

- 2024考纲白皮书

- 2024考前冲刺资料

- 高顿内部名师讲义

- 高顿内部在线题库

摘要:2014年ACCA新大纲考试科目全介绍 FinancialAccounting(FFA/F3) 科目介绍: F3课程主要向学员介绍了财务会计准则、相关会计科目账户建立以及准确财务信息的提供。...

2014年ACCA新大纲考试科目全介绍

Financial Accounting (FFA/F3)

Financial Accounting (FFA/F3)

科目介绍:

F3课程主要向学员介绍了财务会计准则、相关会计科目账户建立以及准确财务信息的提供。

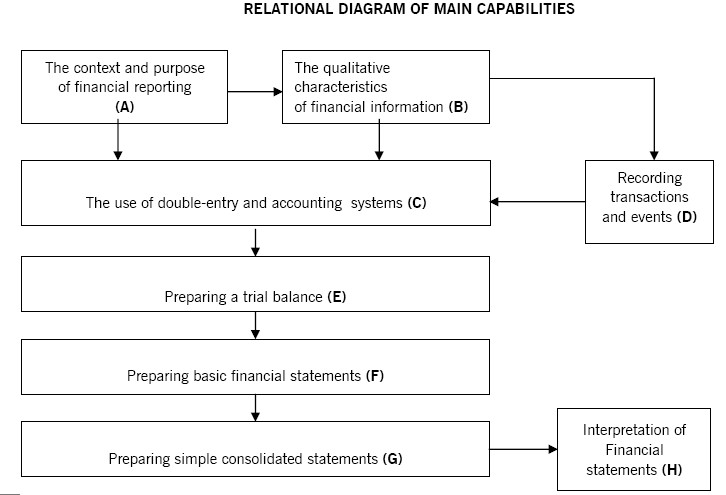

大纲介绍了财务报表编制准备及会计科目建立原则。接着大纲深入展开了公司各类经营行为的会计记录方法,如何使用试算平衡表使用、如何改正账面错误以及需合并报表或非合并报表财务报告的准备工作。之后大纲分出两个重点方向展开,一是要求考生能够对财务报表做一些简单的解读;二是要求学员能够做报表合并。

近几年考试通过率趋势图:

知识结构:

F3课程是ACCA财务会计体系下的基础课程,而财务会计是ACCA主要核心内容,F3也是帮助学员建立财务会计概念财务报表编制、合并、解读的相关知识;因此F3是F7财务报告、P2公司报告的基础。

F3的考试时长为2小时。考生可以采用参加统一笔答考试或在计算机考试中心参与计算机考试两种形式。考试题型由50个单选变为35个单选2个多任务题,单选题共70分,每个任务题15分。

新旧考纲的主要变化:

2014年,主要是考试题型上出现了较大的变化,主要是为了更加接近F7财务报告相关考试要求,缩小了两级考试之间的考试难度。相比之下,F3考试难度增加了,F7反而降低了,在知识结构上,F3的考纲主要是增加了对编制合并报表的要求。加强了与F7的联系,为考生步入F7的学习打好铺垫。 并且, 编制合并报表从简单的选择题到有一定难度的任务题,要求考生熟练掌握报表格式和编制过程。

具体变化点如下:

| Section and areas | Syllables content |

|

B1 a) refer only to IASB Conceptual Framework 出现的qualitative characteristics ,summarized as right: |

Define, understand and apply qualitative characteristics: i) Relevance ii) Faithful representation iii) Comparability iv) Verifiability v) Timeliness vi) Understandability |

| B1 b) replaced with a new outcome including other accounting concepts |

Define, understand and apply accounting concepts [K] i) Materiality ii) Substance over form iii) Going concern iv) Business entity concept v) Accruals vi) Fair presentation |

|

The updated titles of financial statements per IAS 1 Presentation of Financial Statements. |

Income statement’ has been replaced with ‘statement of profit or loss’ and ‘statement of comprehensive income’ has been replaced with ‘statement of profit or loss and other comprehensive income’. |

新考纲--任务题(样题):

Question 1

The following information relates to Geofrost, a limited liability company, for the year ended 31 October 20X7.

Extracts from the statement of profit or loss for the year ended 31 October 20X7

| $’000 |

| Profit before tax 15,000 |

| Less tax 4,350 |

| Profit for the year 10,650 |

| Statement of financial position as at 31 October |

| 20X7 20X6 |

| $’000 $’000 |

| Assets |

| Non-current assets 44,282 26,574 |

| Current assets |

| Inventory 3,560 9,635 |

| Receivables 6,405 4,542 |

| Cash 2,045 1,063 |

| 12,010 15,240 |

| Total assets 56,292 41,814 |

| Equity and liabilities |

| Capital and reserves |

| Ordinary share capital 19,365 17,496 |

| Retained earnings 17,115 6,465 |

| 36,480 23,961 |

| Non-current liabilities |

| Loan 8,000 10,300 |

| Current liabilities |

| Bank overdraft 1,230 429 |

| Trade payables 7,562 4,364 |

| Taxation 3,020 2,760 |

| 11,812 7,553 |

| Total equity and liabilities 56,292 41,814 |

Additional information:

(1) Depreciation expense for the year was $ 4,658,000

(2) Assets with a carrying value of $ 1,974,000 were disposed of at a profit of $ 720,000

Complete the cash flow statement of cash flows for the year ended 31 October 20X7 for Geofrost.

Statement of cash flows for the year ended 31 October 20X7.

| Cash flows from operating activities |

|

$’000 ○ Profit before tax ○ Profit after tax [ ] |

| Adjustments: |

| Depreciation [ ] ○ Add ○ Subtract |

|

Profit on disposal of non-current assets [ ] ○ Add ○ Subtract |

| Inventory [ ] ○Add ○ Subtract |

| Receivables [ ] ○ Add ○ Subtract |

| Payables [ ] ○ Add ○ Subtract |

| Tax paid [ ] ○ Add ○ Subtract |

| Net cash from operating activities |

| Cash flows from investing activities |

|

Payments to acquire non-current assets [ ] ○ Add ○ Subtract |

|

Proceeds from sale of non-currents assets [ ] ○ Add ○ Subtract |

| Net cash from investing activities |

| Cash flows from financing activities |

|

Proceeds from issue of share capital [ ] ○ Add ○ Subtract |

| Repayment of loans [ ] ○ Add ○ Subtract |

| Net cash from financing activities |

|

Net movement cash and cash equivalents [ ] ○ Outflow ○ Inflow Cash and cash equivalents at beginning of period [ ] |

| Cash and cash equivalents at end of period [ ] |

Question 2

Background

On 1 January 20X3 Gasta Co acquired 75% of the share capital of Erica Co for ﹩ 1,380,000. The retained earnings of Erica Co at that date were ﹩ 480,000. Erica Co’s share capital has remained unchanged since the acquisition.

The following draft statements of financial position for the two companies have been prepared at 31 December 20X9.

| Gasta Co Erica Co |

| ﹩’000 ﹩’000 |

| Investment in Erica Co 1,380 0 |

| Other assets 4,500 2,400 |

| Total assets 5,880 2,400 |

| Equity share capital 2,000 1,000 |

| Retained earnings 2,040 660 |

| 4,040 1,660 |

| Liabilities 1,840 740 |

| Total equity and liabilities 5,880 2,400 |

The non-controlling interest(NCI) was valued at ﹩450,000 as at 1 January 20X3.

Task 1

Complete the following to determine the goodwill arising on acquisition.

| Caption |

| ﹩’000 |

| Value of investment at acquisition |

|

Investment in Erica Co held by Gasta Co ○ 480 ○ 660 ○ 1380 ○ 1000 ○ 450 |

|

○ Retained earnings ○ 450 ○ Other assets ○ 1,380 ○ Investment in Erica Co held by Gasta Co ○ 480 ○ Equity share capital ○ 660 ○ NCI as at acquisition ○ 1,000 |

| Total value of investment at acquisition(A) ( ) |

| Fair value of Erica Co’s net assets at acquisition |

|

Equity share capital ○ 480 ○ 1,000 ○ 2,400 ○ 740 ○ 660 |

|

○ Retained earnings ○ 480 ○ Equity share capital ○ 1,000 ○ Liabilities ○ 2,400 ○ Other assets ○ 740 ○ 660 |

| Total fair value of Erica Co’s net assets at acquisition(B) ( ) |

|

Goodwill at acquisition as a formula ○ A-75% of B ○ A+100% of B ○ A-100% of B ○ A+75% of B |

Task 2

Are each of the following statements relating to consolidation correct?

Yes No

The process of consolidation results in a single separate legal entity.

NIC will always feature within the consolidated financial statements.

Goodwill is recalculated using the recent fair values at each reporting period end.

Task 3

Select the formula which correctly calculates NCI as at 31 December 20X9, in accordance with IFRS 10 Consolidated Financial Statements.

○ 25% of net assets at 31 December 20X9.

○ Fair value of NCI at acquisition + 25% of post acquisition profits.

○ Fair value of NCI at acquisition +25% retained earnings as at 31 December 20X9

Task 4

Calculate the following figures which will be reported in Gasta’s consolidated statement of financial position as at 31 December 20X9.

| $’000 |

|

Investment ○ 1380 ○ 0 |

| Other assets ( ) |

| Share Capital ( ) |

| Retained earnings ( ) |

| Liabilities ( ) |

推荐:考生都在用的ACCA资料>>【领取2023ACCA完整资料】 (资料包含ACCA必考点总结,提升备考效率,加分必备)

版权声明:

1、凡本网站注明“来源高顿ACCA”或“来源高顿、ACCA学习帮”,的所有作品,均为本网站合法拥有版权的作品,未经本网站授权,任何媒体、网站、个人不得转载、链接、转帖或以其他方式使用。

2、经本网站合法授权的,应在授权范围内使用,且使用时必须注明“来源高顿ACCA”或“来源高顿、ACCA学习帮”,并不得对作品中出现的“高顿”字样进行删减、替换等。违反上述声明者,本网站将依法追究其法律责任。

3、本网站的部分资料转载自互联网,均尽力标明作者和出处。本网站转载的目的在于传递更多信息,并不意味着赞同其观点或证实其描述,本网站不对其真实性负责。

4、如您认为本网站刊载作品涉及版权等问题,请与本网站联系(邮箱fawu@gaodun.com,电话:021-31587497),本网站核实确认后会尽快予以处理。

分享到:

急速通关计划

ACCA全球私播课

周末面授班

其他课程

- 上一篇:ACCA新大纲解析(F4)

- 网站首页 返回栏目

- 下一篇:ACCA新大纲解析(F2)

报考指南

******ACCA备考机经

价值1288元 考试必备资料 免费领取 高顿ACCA研究院******出品

价值1288元 考试必备资料 免费领取 高顿ACCA研究院******出品

领取ACCA资料包

大家都在看

-

阅读(9579)

阅读(9579) -

阅读(9083)

-

阅读(9068)

-

阅读(8764)

-

阅读(8739)

日排行 • 周排行

- 1 ACCA新大纲解析(P5)

- 2 ACCA新大纲解析(F9)

- 3 ACCA新大纲解析(P3)

- 4 ACCA新大纲解析(F8)

- 5 ACCA新大纲解析(F2)

- 6 ACCA新大纲解析(P2)

- 7 ACCA对于进入咨询行业有什么帮助?

- 8 2012年ACCA新大纲考试F1全介绍

- 9 ACCA新大纲解析(P1)

- 10 ACCA新大纲解析(F3)

- 1 2023年ACCA考试科目通过率排名:哪些科目最容易通过?

- 2 2024年参加12月acca考试带什么?准考证可以打印了吗?

- 3 2024年accaf1裸考能过吗?历年通过率多少?

- 4 定了!2023年acca要考几年能考下来?要考几科才可以拿出去面试?

- 5 2024年acca要考几门?按什么顺序考?

- 6 2023年申请acca免考科目的条件?最多可以免考几门科目?

- 7 2023年哪些大学财会专业比较好?没错了,就是这几所!

- 8 acca学姐来解答2023年acca是什么考试?各科目全称是什么?

- 9 速看!2023年会计学acca是什么意思?一文教你看懂!

- 10 定了!2023年acca考位满了还有可能报上吗?

-

ACCA考试热门词

-

ACCA内部备考资料高顿ACCA为您免费提供全新ACCA资料,包括历年考题、考官报考、考官文章、考纲解析、学霸笔记、内部讲义等,同时还助您了解新学员报名注册指南、机考报考考试引导、OBU&UOL申请攻略等,点击免费获取。

-

- ACCA常见问题

- ACCA推荐阅读

- ACCA考试资讯

- ACCA原创文章

- ACCA学霸分享

- ACCA常见问答

-

- 关于高顿

- 官方白金级认证

- 新******战略合作伙伴

- 前程无忧战略合作伙伴

扫码加入ACCA全国考友群